Table of Contents

Advait Energy Stock Analysis – Key Metrics Snapshot

NSE · Small Cap · Power Transmission, EPC & Green Energy · Mkt Cap ~₹2,210 Cr

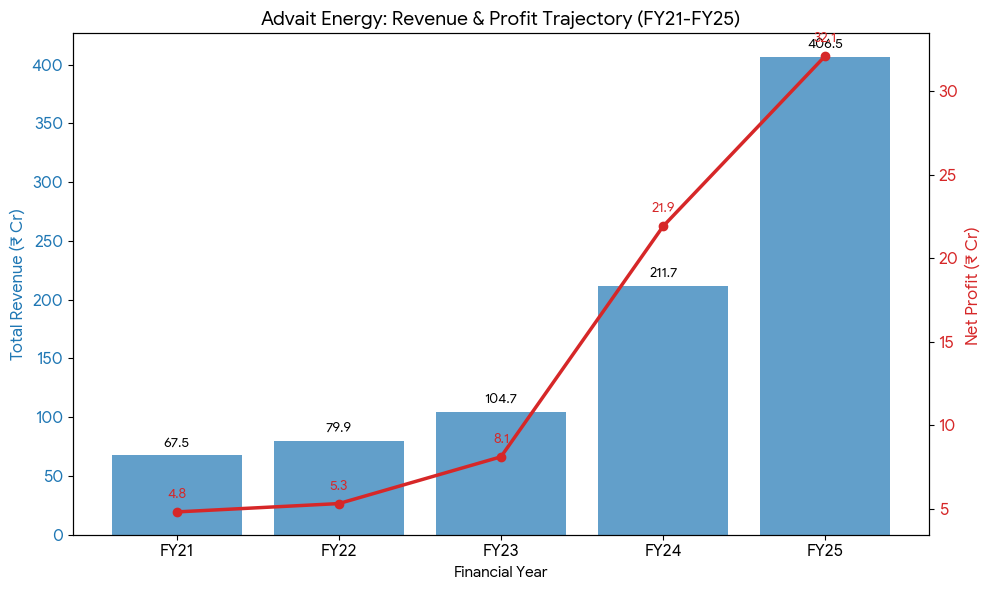

📊 Advait Energy Stock Analysis – Revenue & Profit Trajectory (Hyper-growth phase)

Annual revenue trend:

⚡ Latest Quarterly Snapshot (FY26 momentum)

- Revenue: ~₹210–215 Cr

- YoY growth: ~114%

- Net profit: ~₹16–17 Cr

- Profit growth: ~70% YoY

👉 Growth is still very strong at execution level

📦 Order Book Composition (₹1,048 Cr)

⚡ 1. Power Transmission & Infrastructure (Core segment)

- ~65–70% of order book

- Includes:

- Stringing services

- OPGW (Optical Ground Wire)

- Transmission line EPC support

👉 This is the backbone business driving current revenue visibility.

🌿 2. Substation & Power System Solutions

- ~15–20%

- Includes:

- Substation automation

- Grid connectivity solutions

- Equipment + services

👉 Beneficiary of India’s grid modernisation + renewable integration

🔋 3. Green Energy / Hydrogen / New Initiatives

- ~5–10%

- Includes:

- Early-stage hydrogen infra

- Clean energy transition projects

👉 Small now, but high optionality segment (market assigns premium here)

🌍 4. Exports / International Orders

- ~5–10%

- Projects outside India (Africa, Middle East etc.)

👉 Adds:

- Diversification

- Currency upside potential

📊 Key Insight (Very Important)

👉 ~80–85% of order book = execution-heavy transmission infra

Meaning:

- Revenue visibility = strong

- Margins = likely to remain moderate

🧠 Strategic Interpretation

👍 Positives

- Strong alignment with:

- India’s ₹9–10 lakh crore power infra push

- Renewable evacuation (solar + wind)

- High execution pipeline → supports revenue growth continuation

⚠️ Risks

- Heavy dependence on:

- EPC / service-type contracts

- Leads to:

- Margin pressure

- Working capital intensity

Capex plan — electrolyser manufacturing buildout

Phase 1 — 30 MW assembly

Initial electrolyser assembly plant targeted for commissioning by March 2026. Enables first-mover positioning in India’s green hydrogen supply chain.

Phase 2 — scale to 300 MW

Long-term vision to expand manufacturing to 300 MW capacity. At full scale, could generate ₹200–300 Cr in annual revenue from electrolysers alone.

Total capex outlay

~₹200 Cr planned over 2 financial years for the electrolyser facility. Funded partly through the ₹82 Cr preferential allotment raised in July 2024.

Gujarat green energy MoU

Subsidiary AGPL committed ₹1,450 Cr towards two large green energy projects in Gujarat under GoG facilitation (no GoG equity stake).

Sector tailwinds powering the thesis

Grid modernisation push

India running one of the world’s largest transmission expansion programs. T&D losses near 20% — far above global norms — creating massive reconductoring demand across all states.

HTLS conductor upgrade cycle

Urban density and land constraints making HTLS reconductoring the only practical capacity upgrade on congested corridors. Advait has executed 10,000+ km of live-line work.

Renewable energy integration

Adding 500 GW of renewables by 2030 requires proportional transmission backbone. OPGW cables, substations, and smart grid enablement all benefit Advait’s product suite.

Green hydrogen mission

India’s National Green Hydrogen Mission targets 5 MMTPA production by 2030. Electrolyser demand is the critical bottleneck — Advait is one of very few domestic manufacturers.

BESS & energy storage

MoP launched ₹5,400 Cr VGF scheme for 30 GWh BESS. Advait is progressing large-scale BESS installations at Radhanpur, Gujarat — ahead of most peers in execution.

Make in India / localisation

Government prioritising domestic manufacturing of power equipment. Advait’s ACS wires, OPGW, insulators, and ERS products aligned with import substitution goals.

Growth triggers — near to long term

Order book execution (FY26)

₹1,048 Cr backlog with ~75% expected in next 2–3 quarters. Revenue run-rate already showing hockey stick — Q3FY26 at ₹211 Cr vs full FY25 of ₹399 Cr.

Electrolyser manufacturing revenue

Once the 30 MW Phase 1 facility is commissioned, it creates a new high-margin product revenue stream targeting ₹200–300 Cr per year at full 300 MW scale.

Fuel cell licensing (AVL Austria)

Licensing agreement with AVL List GmbH for fuel cell manufacturing in India opens up the mobility and stationary power market — a multi-decade demand driver.

State DISCOMs — MVCC rollout

Confirmed L1 bidder for DGVCL MVCC turnkey tender; active in PGVCL, PTCUL. DISCOM capex under RDSS is a recurring order pipeline across 25+ states.

Subsidiary: Advait Greenergy IPP

67.1 MWp ground-mounted solar commissioned under IPP mode — transition from pure EPC to asset-owning model adds recurring cash flow and higher valuations.

International expansion

Norway subsidiary (Teco 2030 JV for fuel cells) being wound down strategically; however, the technology IP and manufacturing partnership retained through AVL licensing.

Key risks to monitor

Debtor days at 173 days — elevated working capital risk; long receivable cycles from government utilities can strain cash flow and require higher borrowings.

Valuation premium — stock trades at ~9.6x book and ~56x P/E vs industry P/E of ~20x. Strong execution is already priced in; any delivery miss could compress multiples sharply.

Green hydrogen commercialisation risk — ₹200 Cr electrolyser capex in a nascent market. Demand visibility for electrolysers in India beyond govt mandates remains thin.

Small cap / execution concentration — 128-employee company executing large complex EPC and multi-tech manufacturing simultaneously. Key-man dependency on founder Shalin Sheth.

Disclosure quality — past instances of minor reporting inconsistencies in financial disclosures (flagged by analyst Vijay Malik). Improving but worth monitoring.

Analyst view — conviction with caution

Advait is a rare small-cap that sits at the intersection of three mega-trends: India’s grid modernisation (₹multi-lakh crore spend), green hydrogen (national mission), and renewable integration.

The FY25 revenue near-doubling, a 132% YoY order book surge to ₹1,048 Cr, and an accelerating quarterly run-rate in FY26 point to genuine operating leverage kicking in.

The electrolyser manufacturing bet is high-risk but potentially transformational.

The primary watch items are debtor-day improvement (currently unsustainable at 173 days), capex execution on the electrolyser plant, and any promoter share dilution.

For risk-tolerant investors with a 3–5 year horizon, the risk-reward is skewed positive — but entry valuation at ~56x trailing P/E demands patience for a better price.

Suggested Reading

Vijay Kedia Portfolio, Strategy & Net Worth (2026) – SMILE Investing Explained