Undervalued debt free stocks institutional buying, Undervalued stocks smart money buying, Best debt free stocks long term investing

Finding stocks that combine a

Spotless balance sheet with growing interest from “smart money” is often the closest thing to a “cheat code” in long-term investing.

When a company operates with zero debt, it possesses the ultimate safety net against rising interest rates and economic volatility.

However, the real magic happens when institutional investors— with deep research teams—quietly begin increasing their stakes.

This trend often signals that a stock is not just stable, but significantly undervalued relative to its future growth potential.

In this post, we’re diving into five debt-free gems that the big players are loading up on right now, positioned for massive long-term gains.

Table of Contents

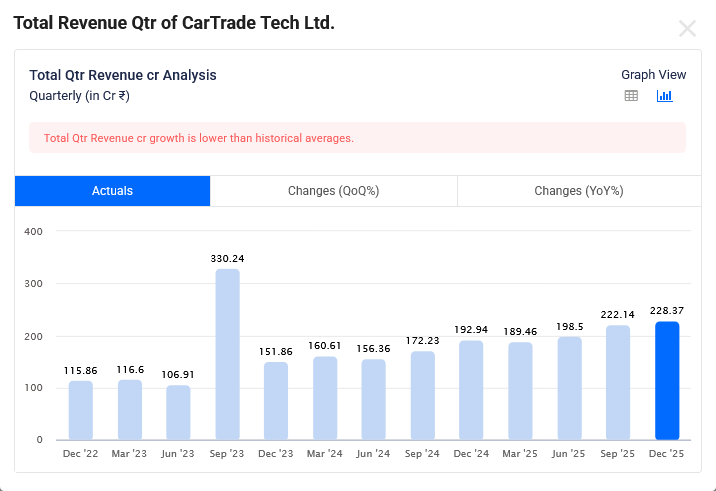

Cartrade Tech

Most people think CarTrade is just a website where you check car prices.

But in 2026, it’s evolved into something much bigger.

After a rocky post-IPO journey, CarTrade Tech is finally turning a massive corner.

Profits are up 76%, they’ve swallowed OLX India, and they’re betting everything on AI.

Today, we’re doing a deep dive: Is this the multibagger you’ve been waiting for, or is the valuation still too high?

Let’s find out.”

Institutional Shareholding Trend

The Business Model: The “Asset-Light” Moat

First, understand why CarTrade is different.

Unlike its competitors who buy and sell cars—which requires massive warehouses and huge debt—CarTrade is Asset-Light.

They don’t own the cars; they own the dataand the platform

The Brands:

CarWale (New cars),

BikeWale (Two-wheelers),

Shriram Automall (Auctions), and

OLX India (Classifieds)

The Advantage:

Because they don’t hold inventory, their gross margins are a massive 85-90%.

When the market goes down, they don’t get stuck with unsold cars.

They just keep collecting ad and lead-gen revenue.”

Growth Trigger 1: The OLX Transformation

The real game-changer was the 2023 acquisition of OLX India.

Before CarTrade, OLX was struggling with losses in its car transaction business.

CarTrade stepped in, shut down the cash-burning parts, and focused on the high-margin Classifieds.

Now, OLX isn’t just about cars.

Over 50% of its revenue comes from horizontal growth—Real Estate, Jobs, and Electronics.

This has turned OLX into a profit machine that fuels the rest of the company.”

Growth Trigger 2: The AI “SuperDost” Revolution

In March 2026, they launched CarTrade Labs.

They’ve moved past simple search bars.

Their new AI agent, ‘SuperDost,’ uses data from 85 million monthly visitors to act as a digital matchmaker.

It’s not just a chatbot.

It handles pricing, loan approvals, and even automates the sales process for dealers.

This increases their ‘conversion rate’—meaning more visitors turn into actual buyers, which means more money for CarTrade.”

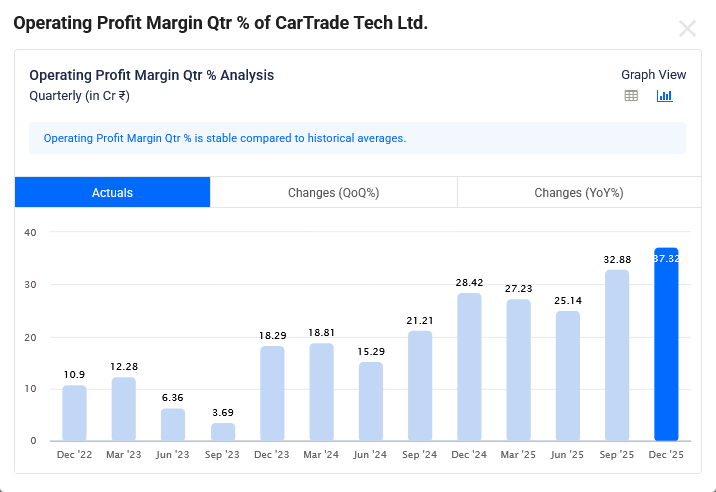

Financials & The “Elephant in the Room” (Valuation)

Let’s look at the numbers.

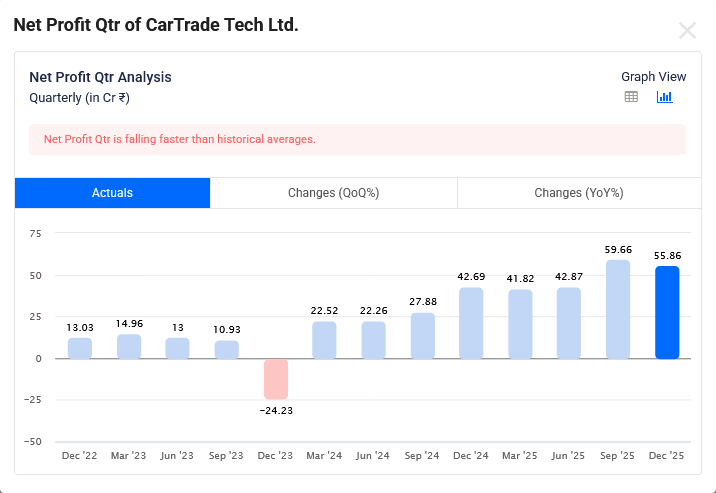

FY25 was a breakout year.

Revenue grew 28%, but Profit exploded by 76%.

They are virtually debt-free, which is rare for a tech company.

Q3 FY 26 Results

CarTrade Tech Dec-2025 Quarterly Revenue is Rs 228 Cr which is growth of 18.4% YoY.

But wait—there’s a catch.

The P/E ratio is currently sitting between 40x and 80x depending on who you ask. That’s expensive.

Conclusion & Final Verdict

So, what’s the verdict?

CarTrade is no longer a ‘speculative’ tech stock; it’s a profitable ecosystem.

If you’re a long-term investor who believes the Indian used-car market will continue to formalize, this is a top-tier pick.

However, because of the high P/E, you might want to wait for dips rather than buying at the peak.

eClerx Services Ltd

Is eClerx Services the best-kept secret in the Indian mid-cap space for 2026?

While the headlines chase the big IT giants, this debt-free KPO powerhouse just posted a 40% jump in net profit and a massive 1-to-1 bonus issue

But with the stock facing some short-term technical pressure, is this a ‘buy the dip’ moment or a falling knife?

Today, we’re doing a deep-dive analysis into eClerx’s financials, their pivot to Agentic AI, and the triggers that could send this stock to new highs.

The ‘Boring’ Numbers are Actually Exciting (Q3 FY 26 Results)

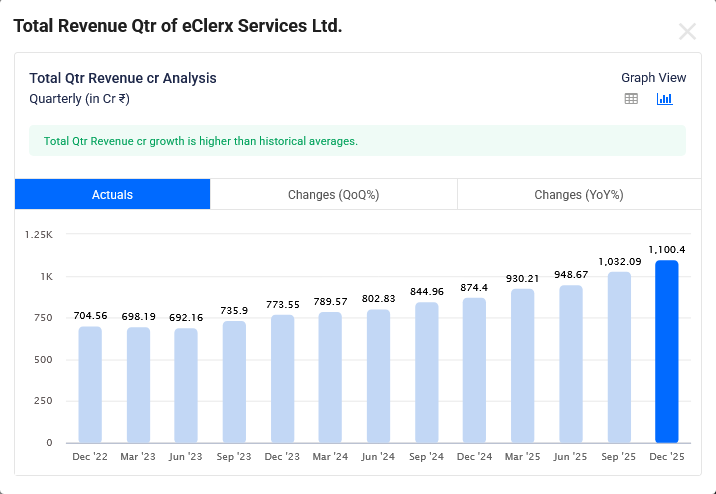

eClerx Services Dec-2025 Quarterly Revenue is Rs 1,100 Cr which is growth of 25.8% YoY.

eClerx Services Dec-2025 Quarterly Net Profit is Rs 205 Cr which is growth of 49.9% YoY.

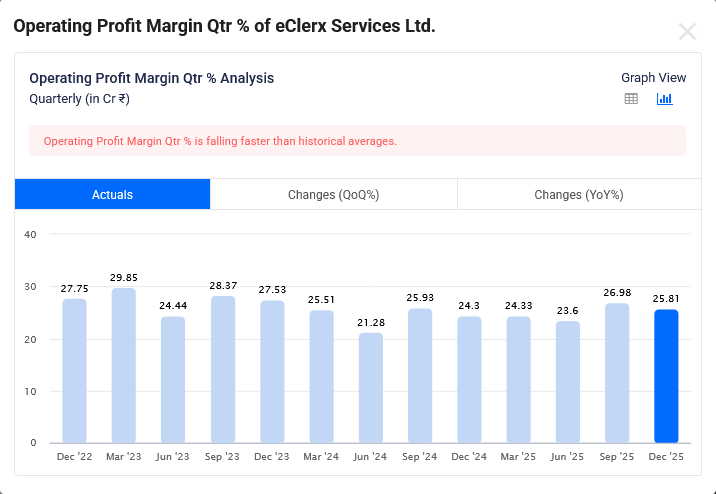

What makes eClerx unique is its efficiency.

We’re looking at EBITDA margins stabilized around 27%.

In a world of rising costs, eClerx is keeping its operations lean while scaling its delivery team to over 21,000 experts globally

The ‘AI-First’ Pivot (Growth Triggers)

The ‘boring’ KPO tag is gone.

eClerx is now an AI-First player.

They’ve launched ‘GenAI360‘ and ‘Roboworx CogniFlows‘—basically autonomous AI assistants that do the heavy lifting for Fortune 500 clients

Why does this matter to you as an investor?

Because it creates non-linear growth.

They can now handle more business without just hiring more people.

Pilot projects are already showing a 15% boost in productivity.

That is pure margin expansion potential.”

The Verdict

So, the verdict? eClerx is a play on quality and cash flow

The Pros: Zero debt, high-end clients, and a massive AI transition

The Cons: Low dividend yield and short-term price volatility

If you’re looking for a dividend play, this isn’t it.

But if you want a high-margin, tech-forward company that aggressively returns value through buybacks and bonuses, eClerx is hard to ignore

Fiem Industries

Most people look at Tata Motors or Mahindra when they think of the EV revolution.

But the real money is often made in the “pick and shovel” companies—the ones making the parts.

Today, we’re breaking down a Tier-1 giant that dominates the lights and mirrors of India’s two-wheelers.

We’re talking about Fiem Industries.

With record margins and a massive shift to LED, is this stock a “buy” at ₹2,000, or is it getting too expensive?

Let’s find out

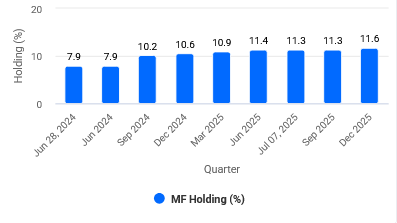

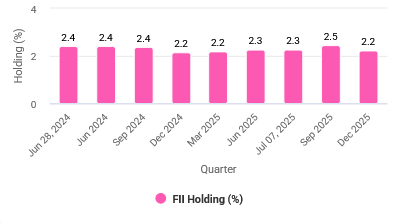

Institutional Shareholding Trend

THE BUSINESS MODEL

Fiem isn’t just a “parts maker.”

They are the backbone for giants like TVS, Honda, and Yamaha. In fact, nearly 97% of their revenue comes from the two-wheeler market.

But here’s the kicker: they aren’t just making old-school bulbs anymore.

Fiem has pivoted hard into LED migration.

Why does that matter?

Because LED lights are more expensive and have better profit margins than traditional bulbs.

Today, LEDs make up nearly 64% of their lighting revenue.

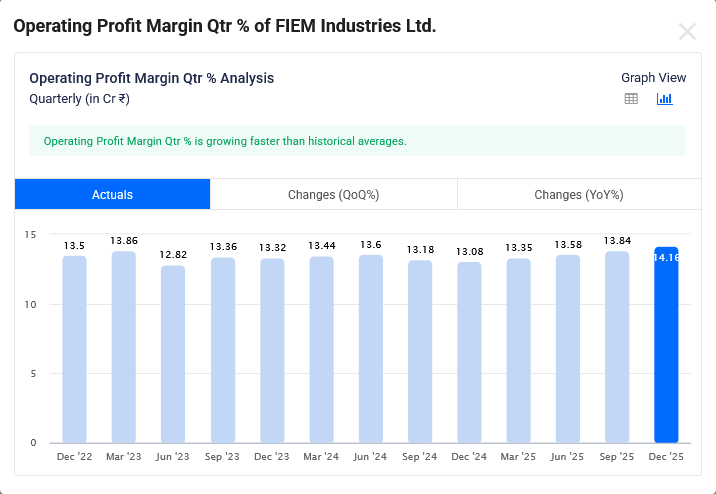

THE NUMBERS (Q3 FY 26)

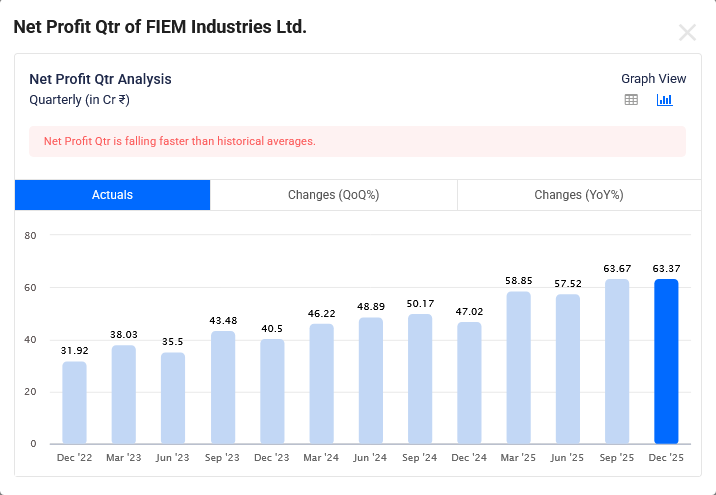

FIEM Industries Dec-2025 Quarterly Revenue is Rs 695 Cr which is growth of 16.4% YoY.

FIEM Industries Dec-2025 Quarterly Net Profit is Rs 63 Cr which is growth of 34.8% YoY.

When you see margins rising while revenue grows, it means the company is getting more efficient.

Their Return on Equity (ROE) is sitting at a healthy 19.7%, and ROCE is a massive 26.8%.

Basically, Fiem knows how to put its capital to work.

THE EV & EXPANSION PLAY

But what about the “Death of Petrol”?

Fiem is ahead of the curve.

They’ve diversified into EV-specific parts like Hub-Motor Assemblies and Motor Controller Units.

Plus, they are finally breaking out of the “two-wheeler only” shell.

They’ve secured orders from Mahindra & Mahindra for heavy hitters like the Scorpio and Bolero.

With a ₹100 crore capex plan for 2026, they are clearly preparing for a much bigger scale.

So, what’s the verdict?

Fiem Industries is a high-quality, high-efficiency player that is perfectly positioned for the LED and EV transition.

If you’re looking for a stable auto-component stock with strong cash flows, this is a top contender.

Sharda Motor Industries Ltd

Every third passenger vehicle on Indian roads carries a secret.

Underneath that shiny chassis is a high-tech exhaust system designed by a company you’ve probably never heard of, but one that dominates the market.”

With a massive 30% market share in exhaust systems and a balance sheet that would make a banker cry tears of joy, Sharda Motor is a silent giant in the auto ancillary space.

But with the EV revolution knocking on the door, can an exhaust king survive?

Today, we’re doing a deep dive into Sharda Motor’s FY26 performance.”

Institutional Shareholding Trend

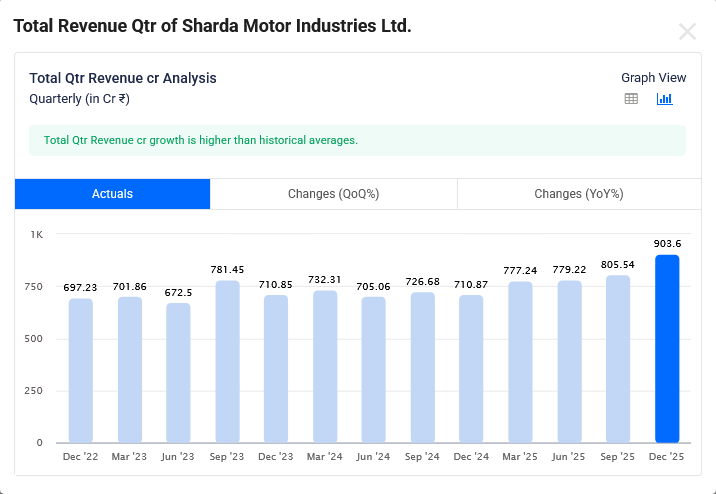

THE NUMBERS (Q3 FY 26)

Sharda Motor Dec-2025 Quarterly Revenue is Rs 904 Cr which is growth of 27.1% YoY.

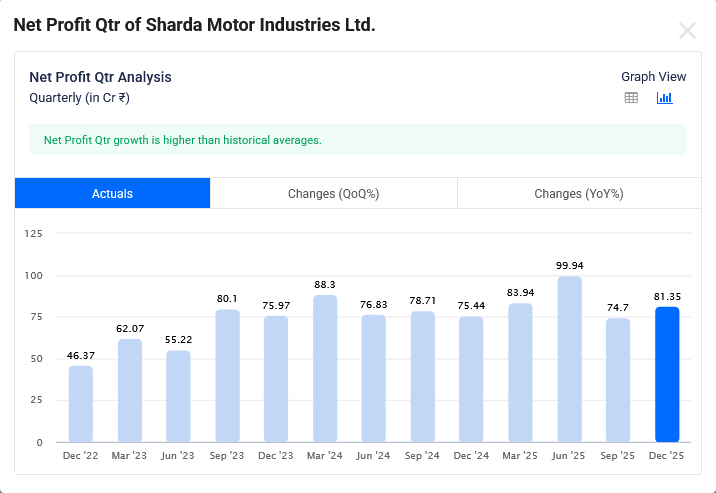

Sharda Motor Dec-2025 Quarterly Net Profit is Rs 81 Cr which is growth of 7.8% YoY.

In Q3 of FY26, Sharda Motor clocked a consolidated revenue of ₹881.6 crore—that’s a massive 28% jump year-on-year.

Their Net Profit also grew 8% to hit ₹81.4 crore.

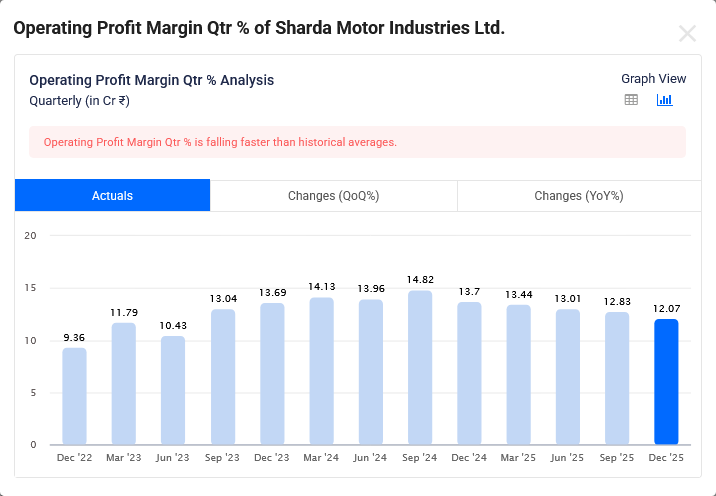

While their EBITDA margins saw a slight dip to 12.1% due to rising costs, the bigger picture is solid: for the first nine months of FY26, they’ve already crossed ₹2,425 crore in revenue.”

THE MOAT (WHY THEY WIN)

What makes Sharda Motor special? Two words: Indigenous Tech.

They aren’t just manufacturers; they are designers.

They are the only Indian company with the tech to build advanced emission control systems in-house.

This has allowed them to become the go-to partner for giants like Mahindra & Mahindra and Hyundai.

They’ve also set up a massive R&D center in Chennai and filed 15 patents in just the last three years.

They aren’t just following the market; they are patenting it.”

THE “TREM-V” TRIGGER

If you’re looking for a short-term catalyst, watch out for April 2026.

That’s when the stricter TREM-V emission norms for tractors are expected to kick in.

Currently, many tractors don’t need complex exhaust systems, but under TREM-V, they will.

This opens up a brand-new, high-margin revenue stream for Sharda Motor.

It’s a massive ‘compliance-driven’ growth story.”

THE ELEPHANT IN THE ROOM (RISKS & EV)

But it’s not all sunshine. Every investor asks: ‘What happens when cars go electric and don’t need exhausts?’

Sharda Motor has two answers.

First, they’ve started a Lightweighting vertical—making suspension parts that even EVs need.

Second, they have a JV with Kinetic Green to manufacture EV battery packs.

However, there is a real risk: 71% of their exhaust revenue comes from just two customers—M&M and Hyundai.

If one of them switches suppliers or slows down, Sharda feels the pain instantly.”

So, the verdict?

Sharda Motor is a cash-rich, debt-free powerhouse that is perfectly positioned to ride the ‘premiumization’ of Indian SUVs and the upcoming tractor norm changes.

While the EV transition is a long-term threat, their pivot into lightweighting and battery packs shows they aren’t sitting idle.

At a time when many companies are struggling with debt, SMIL’s clean balance sheet gives them a massive cushion.”

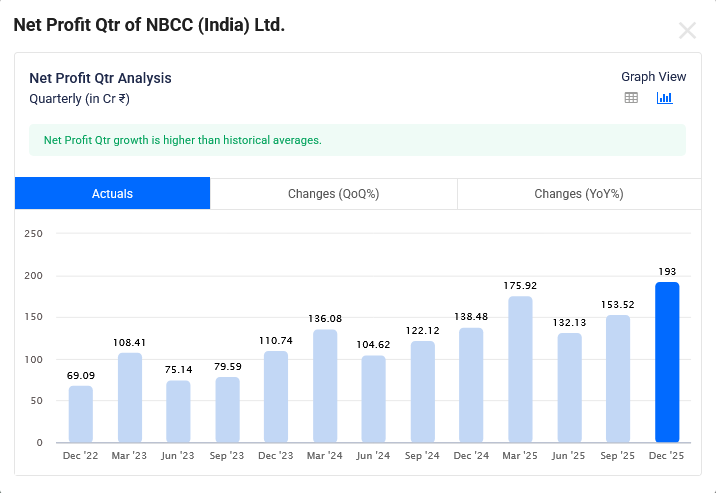

NBCC

What if I told you there’s a debt-free, government-backed company sitting on an order book worth over 1.2 Lakh Crore?

We’re talking about NBCC India.

But while the orders are piling up, the stock price has been under pressure lately.

Is this a ‘buy the dip’ moment or a warning sign?

Let’s dive into a detailed analysis of this Navratna PSU.”

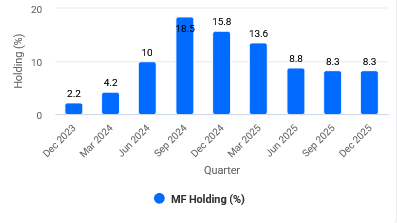

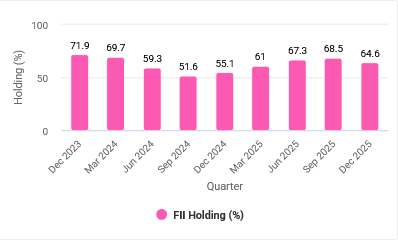

Institutional Shareholding Trend

First, what does NBCC actually do?

Unlike typical builders, they are primarily a Project Management Consultant (PMC).

The PMC Model: They don’t take on the heavy risk of construction themselves; they manage it for the government. This makes them asset-light and virtually debt-free.

The Segments: Over 90% of their revenue comes from PMC. They are the go-to firm for redeveloping government colonies and even finishing stalled private projects like Amrapali.

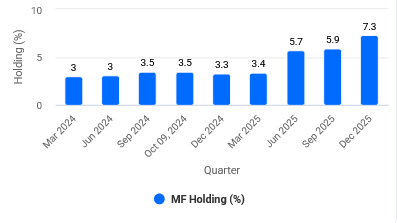

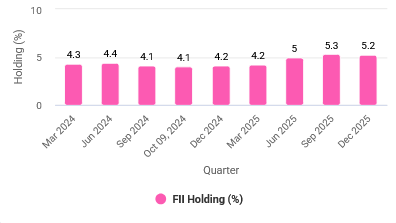

THE NUMBERS (Q3 FY 26)

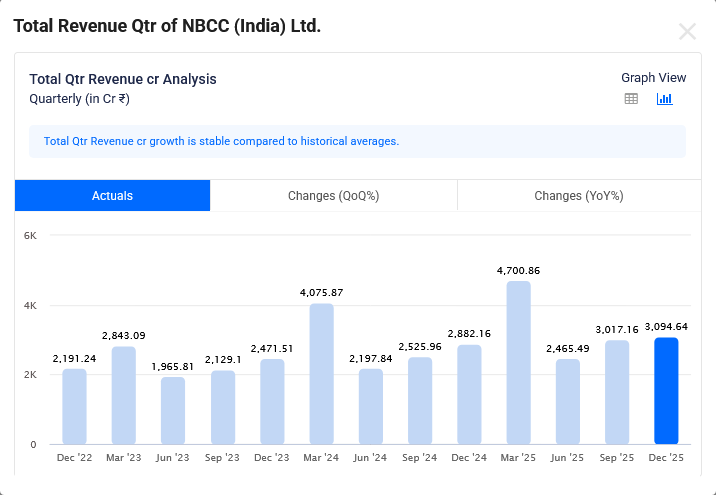

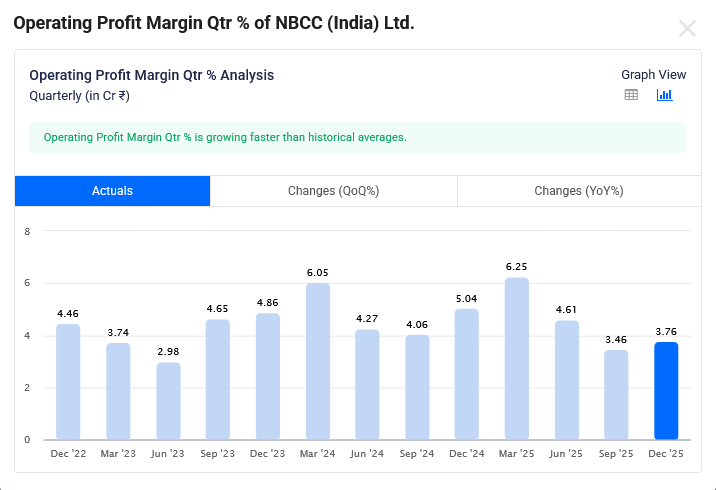

NBCC Dec-2025 Quarterly Revenue is Rs 3,095 Cr which is growth of 7.4% YoY.

NBCC Dec-2025 Quarterly Net Profit is Rs 193 Cr which is growth of 39.4% YoY.