Table of Contents

The Indian IT landscape is witnessing a distinct divergence.

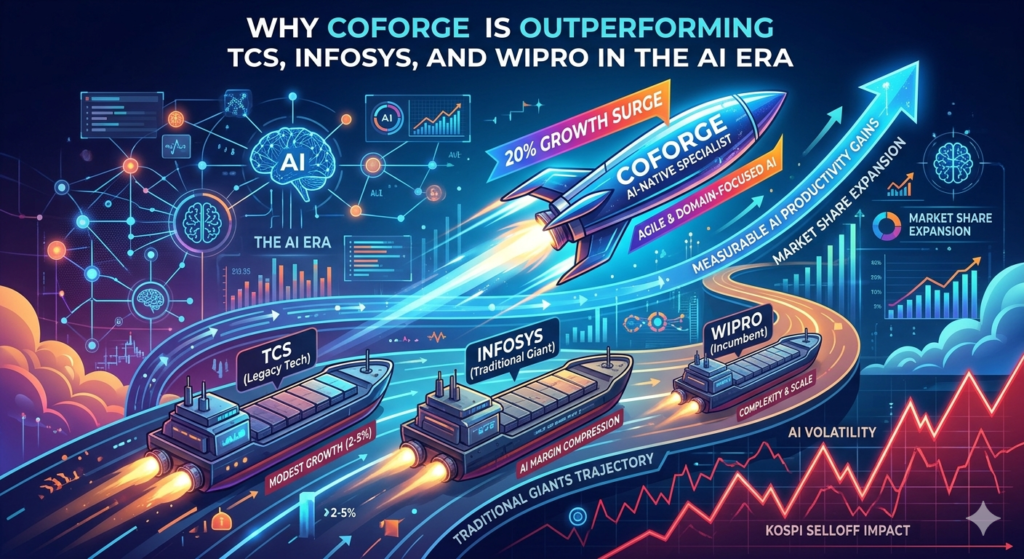

Coforge’s impressive 20% growth surge stands in stark contrast to the conservative trajectories of incumbents like TCS, Infosys, and Wipro—signaling a structural split between legacy giants and nimbler, AI-native specialists.

Although heavy AI expenditures are squeezing margins across the entire sector, Coforge’s agile, domain-specific approach is translating into concrete productivity improvements.

While the Kospi selloff and macroeconomic AI volatility continue to reset market valuations, the defining narrative remains the strategic trade-offs between aggressive growth, bottom-line margins, and expanding market share.

Coforge Limited continues to outclass the broader IT sector, forecasting a near 20% revenue expansion that leaves larger industry peers trailing behind.

This aggressive trajectory is highly structural: roughly 60% to 70% of the growth stems from distinct, client-specific digital transformation victories, while the remaining 30% to 40% capitalizes on a macro-level sector recovery.

A stellar Q1 FY26 performance saw the firm secure five landmark deals, culminating in a historic $507 million order intake and expanding its executable order book by 46.9% year-on-year to $1.55 billion.

This momentum is further validated by strong account farming, as sequential growth among top 5 and top 10 clients reached 25.1% and 15.7%, respectively.

This growth trajectory stands in stark, unflattering contrast to India’s legacy IT triumvirate.

Tata Consultancy Services managed a muted 1.67% year-on-year revenue expansion, while Infosys posted a moderate 9.37% gain.

Meanwhile, Wipro continued to face headwinds, reporting a 4.03% revenue contraction.

These numbers underscore a broadening structural rift between agile mid-tier specialists and stagnant legacy conglomerates.

While TCS continues to demonstrate massive distribution scale by commanding a $9.4 billion TCV, the underlying composition of these deals tells a different story. A heavy concentration of this backlog is tied to vendor consolidation initiatives. Because these engagements involve taking over existing legacy footprints rather than launching new, high-velocity projects, they act as defensive plays that delay immediate revenue realization.

Divergent operational realities are taking center stage among Tier-1 Indian IT firms.

Reflecting improved demand visibility and stable client spending, Infosys upgraded its full-year FY26 constant currency revenue growth projections upward to a 3–3.5% band.

In contrast, Wipro’s recovery timeline remains elongated despite striking gold in pipeline generation.

The Bengaluru-based company logged a stellar $5.0 billion in total contract value (TCV)—marking an impressive 50.7% expansion relative to the previous year.

Yet, these paper wins have failed to translate immediately into macro growth, as ongoing delivery and integration headwinds actively dilute its historic deal-making streak.

This performance disparity highlights two fundamentally different client spending patterns across the industry.

Larger IT conglomerates are absorbing the brunt of macroeconomic headwinds, as enterprise clients postpone discretionary digital investments to prioritize immediate cost optimization.

Conversely, Coforge continues to insulate its top line by dominating high-value verticals—specifically BFSI, travel, and healthcare—where niche domain expertise remains highly billable.

This divergence was temporarily overshadowed by broader market volatility during the June 2026 Kospi capitulation.

Triggered by compounding global AI valuation corrections and South Korea’s exclusion from the MSCI Developed Markets index, the shockwaves caused the Nifty IT index to contract 1.80%, pulling TCS down 2.24% and Infosys down 2.99%.

However, the underlying fundamentals of the Indian tech sector triggered an immediate turnaround.

A subsequent 4% market rally indicates that institutional capital has discounted the systemic volatility, shifting its focus back to imminent Q1 earnings results.

The AI Innovation Paradox: Why Bottom-Line Profits Are Lagging Behind Tech Breakthroughs

A structural lag persists between initial AI deployment expenditures and long-term top-line revenue realization.

AI-driven efficiencies are being transferred directly to buyers at the negotiation table rather than being retained as operational profit.

As Q1 FY26 earnings results reveal, service providers are actively sharing their technological productivity dividends with enterprise clients to defend market share—a defensive necessity that firmly caps overall margin expansion.

The financial reality of building competitive AI capabilities is becoming increasingly clear.

During the final quarter of FY26, Tata Consultancy Services (TCS) absorbed a substantial 100 basis point margin contraction exclusively driven by AI expenditures.

Infosys navigated similar headwinds, absorbing a 40–50 bps operational hit from AI infrastructure costs, though it managed to successfully defend its 21% operating margin baseline.

In contrast, Wipro accelerated funding for its proprietary Wipro Intelligence platform and specialized AI-native business division.

These heavy front-loaded investments have intensified margin pressures, dragging Wipro’s operating margin down to 17.3%—marking the lowest profitability tier among its immediate peers.

In sharp contrast to legacy conglomerates, Coforge demonstrates how tactical agility can accelerate value capture.

Although its current 13.2% EBIT margin remains structurally lower than the Tier-1 giants, the firm’s profitability is on an upward trajectory fueled by tangible operational optimizations.

Rather than relying on long-term projections, Coforge is logging immediate dividends: a 30% to 40% reduction in employee support query resolution times, a 40% to 60% automation rate in manual financial analysis, and a 25% to 35% productivity expansion across its AI-enabled hybrid delivery frameworks.

Backed by a disciplined $5.5 million deployment in AI infrastructure and over 290,000 hours of workforce retraining, Coforge has effectively shortened the cash conversion cycle on innovation.

A clear causal relationship has emerged across the sector: front-loaded AI research and development and intensive workforce upskilling are squeezing near-term operating margins universally.

Yet, the strategic toolkits deployed by these firms vary immensely. TCS successfully leverages its massive corporate scale to absorb these shocks, comfortably maintaining the industry’s highest absolute margin profile at 25.3% despite its recent 100 bps contraction.

Infosys has adopted a balanced approach, offsetting localized AI cost pressures by demanding premium pricing tiers for its highly differentiated digital transformations.

Conversely, Wipro is absorbing the most significant margin stress, demonstrating a clear willingness to compromise near-term profitability to capture and defend long-term market share.

Breaking away from the large-cap narrative, Coforge capitalizes on its lean organizational structure and AI-native architecture, engineering genuine margin expansion through realized operational efficiencies rather than raw legacy scale.

Growth Acceleration vs. Margin Defense: The New IT Playbook

The recent 4% surge across Indian IT equities immediately preceding TCS’s Q1 financial release represents technical bargain hunting rather than a fundamental demand reversal.

This localized bounce follows a historic macro correction where the broader sector saw over ₹17 lakh crore in market value evaporate.

Bellwether valuations experienced massive compression during this period: TCS retraced 56% from its August 2024 peak, Infosys shed nearly 50% from its December 2024 high, and Wipro dropped 54%.

While short-term capital is positioning for the upcoming earnings cycle, baseline operational expectations remain highly conservative.

Consensus brokerage projections point to flat or negative sequential revenue expansion across large caps, though Infosys and Tech Mahindra are tipped to show superior relative strength.

Macro headwinds and structural AI concerns continue to drive severe valuation multiple compression across tech equities.

Compounded by the recent Kospi capitulation, the Nifty IT index has severely underperformed the broader market by 20% since January 2026, primarily due to aggressive P/E derating linked to long-term AI disruption anxieties.

Institutional analysts are rapidly pricing in these risks; Kotak Institutional Equities revised its generative AI pricing deflation models to the upper limit of its 3%–3.5% range, cutting fair value estimates by as much as 21% across its coverage universe.

Amplifying this caution, Morgan Stanley downgraded Tata Consultancy Services (TCS) to Equal-Weight.

The firm noted that TCS’s valuation premium relative to Accenture had ballooned past 40%, signaling a broader overvaluation risk for Indian IT large caps.

The muted start to the FY27 fiscal year stems primarily from transient cyclical headwinds rather than deep structural erosion.

Unified management commentary reveals that project delays are the result of macro instability, trade policy friction, and geopolitical conflicts rather than a systemic decline in IT demand.

Robust contract backlogs across the sector provide definitive proof that enterprise technology spending has been deferred rather than permanently cancelled.

This pipeline resilience is led by TCS commanding a $9.4 billion pipeline, Infosys securing $3.8 billion, and Coforge reinforcing its footprint with a $1.55 billion order book.

Looking ahead, HSBC Global Research anticipates a powerful demand inflection point.

Fueled by a stabilizing US macroeconomic climate and accelerating enterprise AI deployments, the firm forecasts that this latent demand will unlock a 200 to 300 basis point expansion in top-line revenue growth for the industry.

AI-Native vs. AI-Add-On: Why Coforge is Outrunning Traditional Tech

There is no mystery behind Coforge’s near 20% revenue acceleration.

Rather than relying on sector tailwinds, the mid-cap specialist’s growth premium is the direct consequence of divergent strategic execution.

While its larger Tier-1 peers remained anchored to broad legacy frameworks, Coforge deliberately positioned itself around agile, specialized verticals, proving that its outperformance is entirely structural rather than coincidental.

While larger industry peers treat AI as a superficial layer on top of legacy service models, Coforge operates on an AI-first architecture, completely embedding automation within its delivery pipeline.

According to its Q4 FY26 investor presentation, Coforge’s structural advantage is anchored by its proprietary “mod-squad” delivery model.

By organizing AI agents and human specialists into highly optimized, pod-based units, the company achieves a 40% to 50% acceleration in time-to-market.

Crucially, this setup allows Coforge to transition to outcome-based pricing structures, successfully dismantling the bloated, multi-layered delivery pyramids that legacy incumbents are finding impossible to unwind.

The structural outperformance at Coforge is underpinned by its proprietary Coforge OneAI platform, which boasts more than 60 pre-built, production-grade workflows engineered specifically for regulated verticals.

Rather than deploying commoditized, horizontal AI solutions, the firm leverages highly specialized industry IP to construct resilient competitive moats.

This deep domain strategy has allowed Coforge to cultivate exceptional client concentration across its core segments: BFSI anchors 26.5% of the portfolio, followed closely by Travel at 23.0%, Insurance at 15.0%, and Healthcare at 10.8%.

This systemic integration into client operations has yielded an industry-leading 95.5% repeat business ratio.

The commercial validity of this approach is further underscored by aggressive account mining, as evidenced by a remarkable 45.8% and 40.4% growth surge among its top 5 and top 10 client buckets, respectively.

India’s legacy Tier-1 conglomerates are navigating entirely different strategic choices, illustrating that there is no uniform response to the AI era.

Tata Consultancy Services (TCS) consistently prioritizes long-term margin defense over aggressive top-line acceleration [TCS].

By systematically restructuring AI efficiency gains straight into initial deal values [TCS], its margin-disciplined framework reliably shields the firm from gradual profitability erosion.

Infosys has implemented a balanced, dual-track operational strategy .

The company absorbs modest near-term margin headwinds to sustain its aggressive AI development pipeline while focusing heavily on cultivating shared productivity frameworks alongside its enterprise buyers .

In stark contrast, Wipro is executing the sector’s most aggressive volume-capture campaign .

Operating under an “AI-first, AI-everywhere” mandate [Wipro], the Bengaluru-based firm is actively weaponizing its balance sheet—willingly undercutting its own target margin baselines to isolate and secure business-critical customer accounts .

Underlying client concentrations and localized geographic footprints explain the vast majority of the industry’s recent growth divergence.

Coforge has strategically anchored its portfolio within highly regulated industries featuring rigid, non-discretionary transformation requirements—safeguarding its pipeline from the sudden budgetary cutbacks denting larger competitors .

As disclosed in its Q4 FY26 investor report, this advantage is further amplified by a highly resilient geographic revenue distribution .

The Americas region comprises 56.9% of the firm’s total mix, registering an exceptional 34.6% year-on-year expansion .

Similarly, operations in EMEA represent 28.9% of the business at a 14.3% growth rate, while the Rest of World cluster surged by 49.9% .

In contrast, India’s Tier-1 tech conglomerates carry outsized exposure to highly cyclical consumer verticals and static geographic concentrations, directly compounding their vulnerability to global macroeconomic fluctuations.

The Great Decoupling: Indian IT Has Split into Two Distinct Sectors

The overarching narrative of the Indian IT sector has ceased to be monolithic.

Coforge serves as a blueprint for an AI-native future: a lean organization defined by deep vertical expertise, outcome-based monetization, and aggressive top-line acceleration .

Conversely, TCS, Infosys, and Wipro anchor the industry’s traditional present, leveraging unmatched distribution scale and disciplined cost protection to manage their long-tail structural transformations .

While both operational models offer distinct value propositions to institutional investors, their long-term trajectories are fundamentally decoupling.

For market participants, the investment implications of this structural divide are increasingly clear.

Coforge’s premium valuation remains highly justified by its native architecture and a specialized operational framework that is translating innovation into expanding margins .

Conversely, while its larger Tier-1 peers offer attractive defensive value following a historic market-wide derating , their deeply entrenched operational constraints will likely cap top-line acceleration until their legacy transformations are fully finalized.

While the systemic volatility triggered by the Kospi capitulation has opened distinct buying opportunities, long-term capital allocation must remain highly selective.

The definitive test for the sector will rest on imminent Q1 earnings prints and forward-looking management commentary—specifically regarding near-term AI revenue scaling, margin stabilization timelines, and the true conversion velocity of backlogged deal pipelines.

The primary timeline for structural AI disruption is projected to run through FY26 to FY28, with an industry-wide demand recovery slated from late FY28 onward.

Tech companies that successfully navigate this high-friction transition—whether by leveraging an AI-first framework like Coforge [Coforge] or a strictly disciplined structural transformation like TCS [TCS]—are poised to emerge with superior operating leverage.

Conversely, organizations unable to bridge the gap between legacy and automated delivery models risk a permanent erosion of their market position.

While the recent 4% market rally indicates institutional capital is looking toward long-term stabilization, imminent quarterly metrics will serve as the definitive filter separating high-conviction assets from structural laggards.

Coforge Share Price

Suggested Reading

Vijay Kedia Portfolio, Strategy & Net Worth (2026) – SMILE Investing Explained